New Faculty: Professor Minju Lee

As of August 1, 2025, Professor Minju Lee joined us as a new faculty member. Received a doctoral degree in 2021 from Yale University, Professor Kim worked at School of Mathematics of IAS(Member, 2021-2022) and University of Chicago(Dickson Instructor, 2022-2025). He specializes in Homog...

New Faculty: Professor Beomjun Choi

As of July 1th, 2025, Professor Beomjun Choi was appointed as an Associate Professor. Professor Choi received his Ph.D. from Columbia University in 2019. He served as Assistant Professor at POSTECH (2021-2025). He majored in Geometric Analysis, Differential Geometry, Partial Differen...

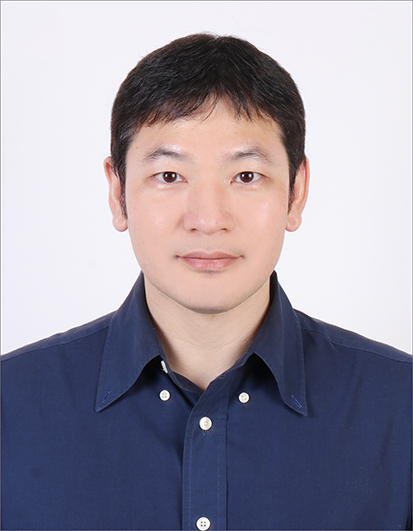

New Faculty: Professor Donghan Kim

As of August 1, 2024, Professor Donghan Kim joined us as a new faculty member. Received a doctoral degree in 2020 from Columbia University, Professor Kim worked at University of Michigan(Assistant Research Professor, 2021-2024). He specializes in Mathematical Finance and Stochastic Anal...

Prof. Jae-Kyung Kim receives a citation from the Minister of Science and Technology and ICT

Prof. Jae-Kyung Kim of Woori Department has been awarded the 'Ministerial Citation' by the Ministry of Science and ICT. In 2017, Prof. Kim received a research grant from the Human Frontier Science Program (HFSP), an international organization known as the Nobel Prize Fund, to conduct resea...

New Faculty: Professor Jiewon Park

Received a Ph.D. degree from MIT in 2020, Dr. Jiewon Park joins the Department of Mathematical Sciences on August 1, 2023 as an assistant professor. Prior to KAIST, Dr. Park worked as Gibbs Assistant Professor at Yale University from July 2021 to June 2023. She specializes in Differenti...

New Faculty: Professor Youngjoon Hong

As of August 1, 2023, Professor Youngjoon Hong was appointed as an Associate Professor. Professor Hong received his Ph.D. from Indiana University in 2015. He served as Assistant Professor at Sungkyunkwan University (2021-2023). He majored in Scientific Computing and Machine Learning.

New Faculty: Professor Woojin Kim

As of July 1, 2023, Professor Woojin Kim joined us as a new faculty member. Received a doctoral degree in 2020 from Ohio State University, Professor Kim worked at Duke University(William W.Elliott Assistant Research Professor, 2020-2023). He specializes in Applied and Computational Topo...

2023 MWC Du-myeong Scholarships and Fellowships Award Ceremony

On Thursday, May 4, 2023, the Du-myeong (Two) Scholarships and Fellowships Awards Ceremony of MWC (Miwon Corporation) was held at the Education 4.0 Lecture Room of the Department of Mathematical Sciences at KAIST. Second-year student Kwon Dohyeong received a scholarship of KRW...

Scientists re-writes FDA-recommended equation to improve estimation of drug-drug interaction

Drugs absorbed into the body are metabolized and thus removed by enzymes from several organs like the liver. How fast a drug is cleared out of the system can be affected by other drugs that are taken together because added substance can increase the amount of enzyme secretion in the body. This dr...

Professor JungHwan Park and Dr. Sungkyung Kang’s work featured by Quanta

Professor Park and Dr. Kang’s recent article “The (2,1)-cable of the figure-eight knot is not smoothly slice” was featured in Quanta magazine. The work is joint with Irving Dai, Abhishek Mallick, and Matthew Stoffregen. Sungkyung Kang got a bachelor degree in 2014 and a master’s degree in 2015 fr...

Department Seminars and Colloquium

Stefan Friedl (Universität Regensburg)Topology Seminar

Twisted homology and Reidemeister torsion #3

Stefan Friedl (Universität Regensburg)Topology Seminar

Twisted homology and Reidemeister torsion #4

MYUNG-SIN SONG (Southern Illinois University)Applied mathematics

Operator theory, kernels, and feedforward neural networks

Kihyun Kim (Seoul National University, Department of Mathemati)Colloquium

On classification of bubbling dynamics for critical PDEs

Giannis Platis (University of Patras)Topology Seminar

Horizontal curvatures of surfaces in 3-dimensional, contact sub-Riemannian Lie groups

Graduate Seminars

SAARC Seminars

PDE Seminars

IBS-KAIST Seminars

Graduate School of AI for Math Seminar

Conferences and Workshops

Student News

Bookmarks

Research Highlights

Bulletin Boards

Problem of the week

We want to find the maximum area of two disjoint, congruent tiles that can be packed inside a right triangle, one of whose angles is \( \pi/6 \) (30 degrees). What would be the maximal coverage of the right triangle by the tiles? (4 points will be given to the one with the best answer, and 3 points for the next four best answers.)

KAIST Compass Biannual Research Webzine

We want to find the maximum area of two disjoint, congruent tiles that can be packed inside a right triangle, one of whose angles is \( \pi/6 \) (30 degrees). What would be the maximal coverage of the right triangle by the tiles? (4 points will be given to the one with the best answer, and 3 points for the next four best answers.)